The Chicago Board Options Exchange’s (CBOE) Volatility Index (VIX), is a popular measure of volatility based on the S&P 500’s index options. It is a “a real-time index that represents the market’s expectations for the relative strength of near-term price changes of the S&P 500 Index (SPX)” (Investopedia). It is used to determine the market’s volatility, both the upside and downside, over the coming 30 days, and is a popular resource for investors when analyzing the market’s action.

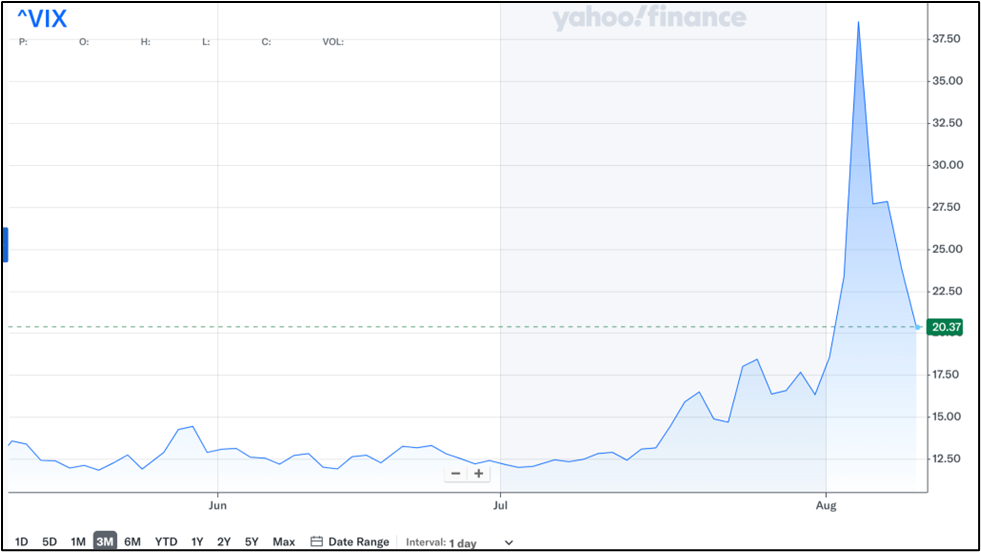

On Monday (8/5/24), the stock market performed poorly due to rising fears of a recession in response to the recent jobs report, worries that the Federal Reserve has gone too far in keeping rates high, and Japan increasing interest rates for the first time in 17 years. On Friday (8/2/24), the VIX reached an 18-month high and was up 29.23% at market close (higher VIX means higher volatility). As you can see in Figure 1, the VIX reached an 18-month high on August 2th, which is indicative of the record-breaking spike from Monday, August 5th.

Figure 1: The VIX’s 3-month performance as of August 12th, 2024

The recent job report revealed that unemployment is now at the highest rate since October 2021, at 4.3% as of August 2nd. This, along with the realization that the Fed may have gone too far in maintaining higher restrictive short-term interest rates, hindered the performance of the S&P 500 and led the VIX to increase. Japan’s decision to raise interest rates for the first time in 17 years also influenced this spike. Carry trades are common through the Yen currency, due to Japan’s export-driven economy, which helps investors borrow money in Japan with lower interest rates and get higher returns on foreign investments such as US bonds. However, with Japan’s interest rates and the US expecting a rate cut, the US dollar will become less valuable and has caused shifts in the international markets.

Although the VIX spiked, it is important to remember to not make sporadic and emotional decisions that may impact your portfolio and lessen your wealth. Although a recession may be near, it is important to trust your financial portfolio and stick to long-term equity-based portfolio management. The economy cycles, and you can’t predict its performance, which is why it is imperative to choose stocks with strong earnings, solid cash flow, and little or no debt.

By Sam Bassett