Congratulations! You are recently retired and all your saving and planning over the years have finally paid off. You feel optimistic about your future and you are deciding whether to start playing more golf or maybe try out tennis at the local club. However, before you pull out your racquet or driver you must first plan for your spending throughout retirement.

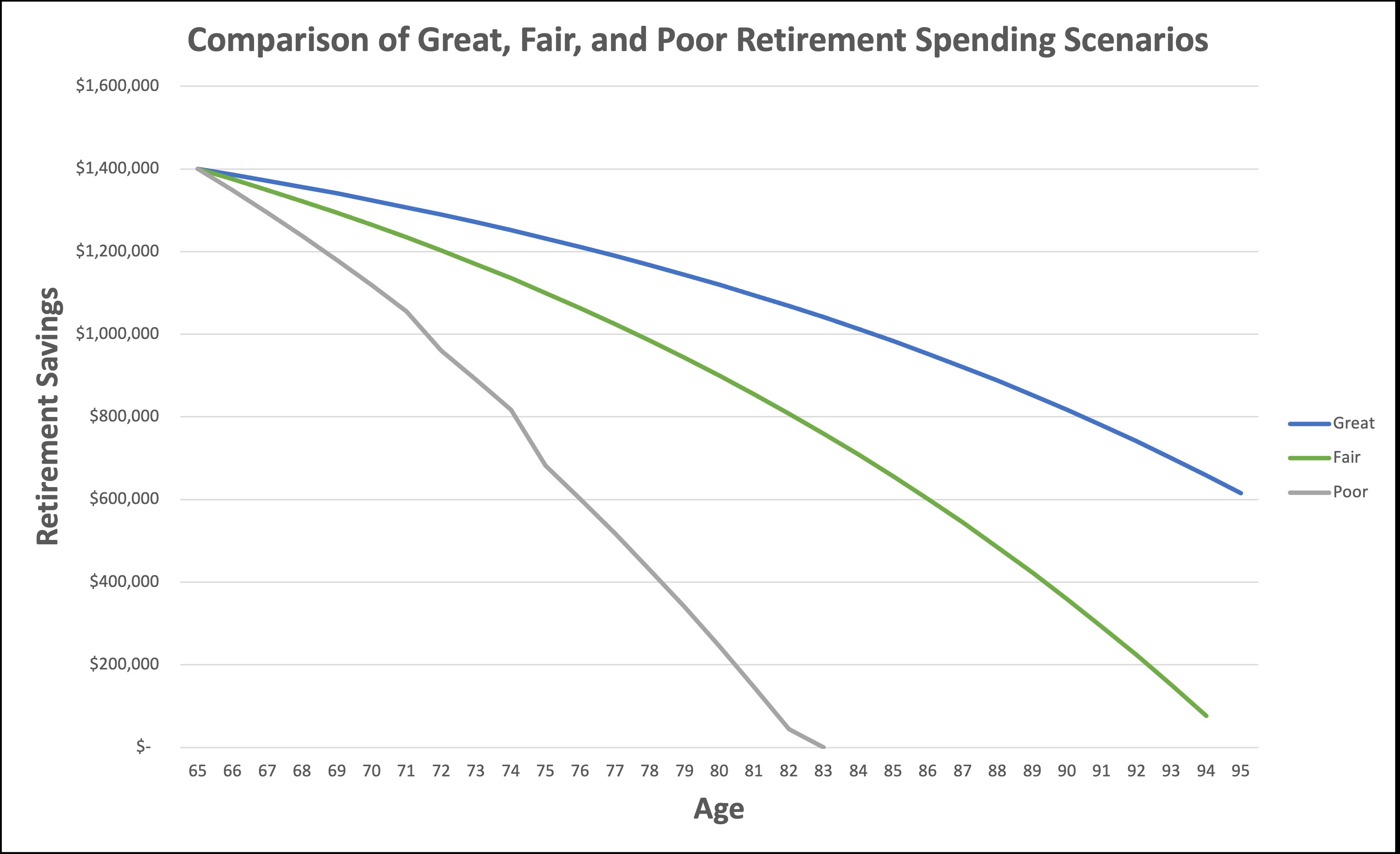

Budgeting your retirement savings and plan for your withdrawals is crucial to enjoying life once you have successfully retired. Let’s look at three different examples of great savings, fair savings, and poor savings throughout retirement. Jack Didgreat, Jill Didfair, and John Didpoor are three individuals who each accumulated $1,400,000 in retirement savings by the start of their retirements at 65 years old, and generate a conservative investment return of 4% annually.

| Investment Account | $300,000 | (dividends & capital gains) |

| Traditional IRA | $700,000 | (distributions taxable) |

| Roth IRA | $50,000 | (non-taxable) |

| Pawleys Dividend Fund | $300,000 | (dividends & capital gains) |

| Bank savings | $50,000 | (interest taxable) |

| $1,400,000 |

Here are the distributions and spending stories of the $1,400,000 for all three individuals:

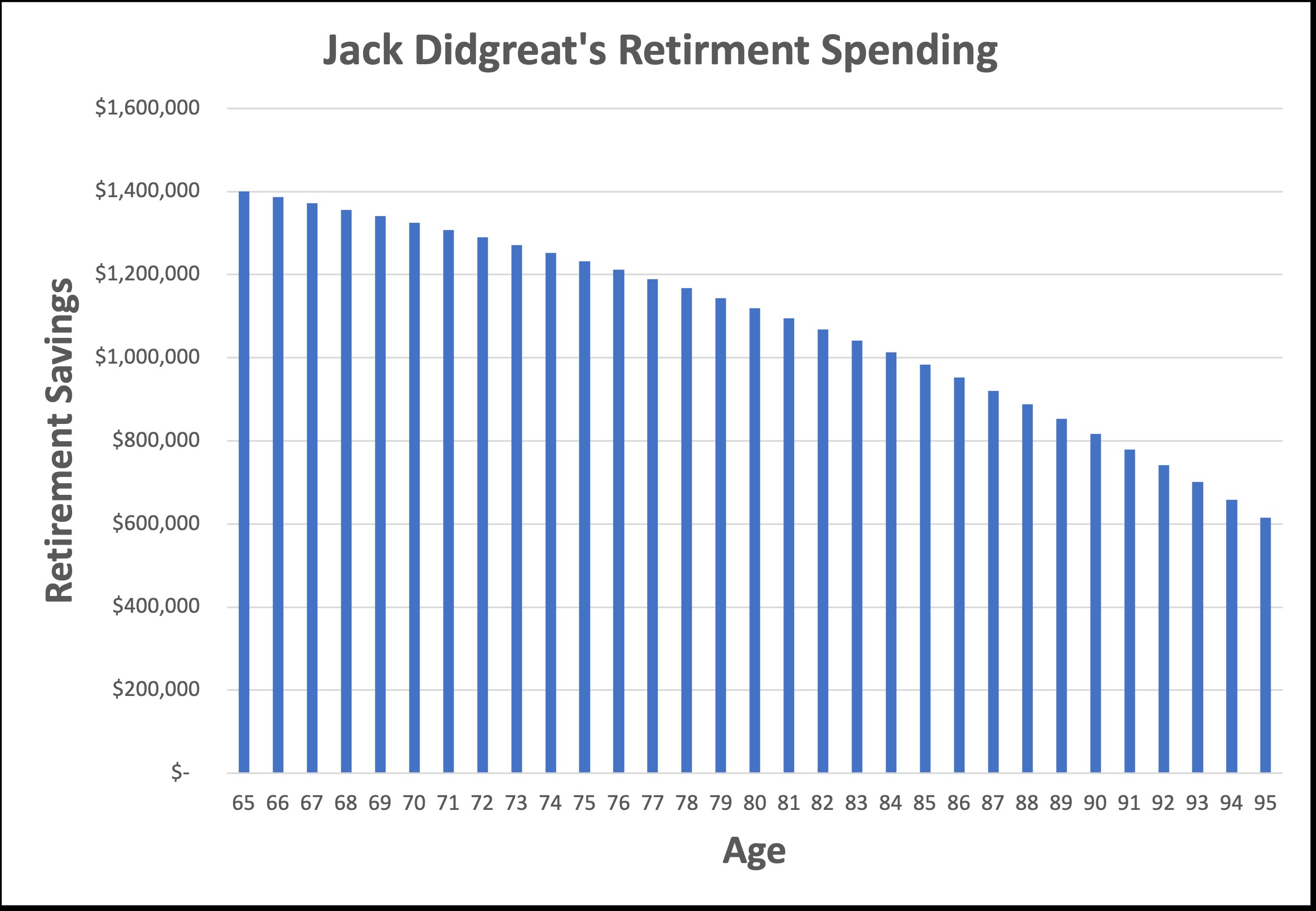

Jack Didgreat decided he would withdraw $2,500 monthly and an additional $40,000 each year. When he planned it out, he would still have $569,403 at 96 years old, giving him financial room for other purchases throughout retirement, and safety for whatever life throws at him.

Jill Didfair decided to plan her savings like Jack, but decided to withdraw $3,000 monthly and an additional $45,000 each year. Doesn’t seem like that much more than her friend Jack, right? Jill Didifair would actually run out of her savings at 94 years old, which does not give her much financial room throughout retirement and leaves her with nothing to support herself past 94. It is crazy how Jill spending an extra $500 dollars each month and an extra $5,000 each year leaves her with nothing compared to Jack!

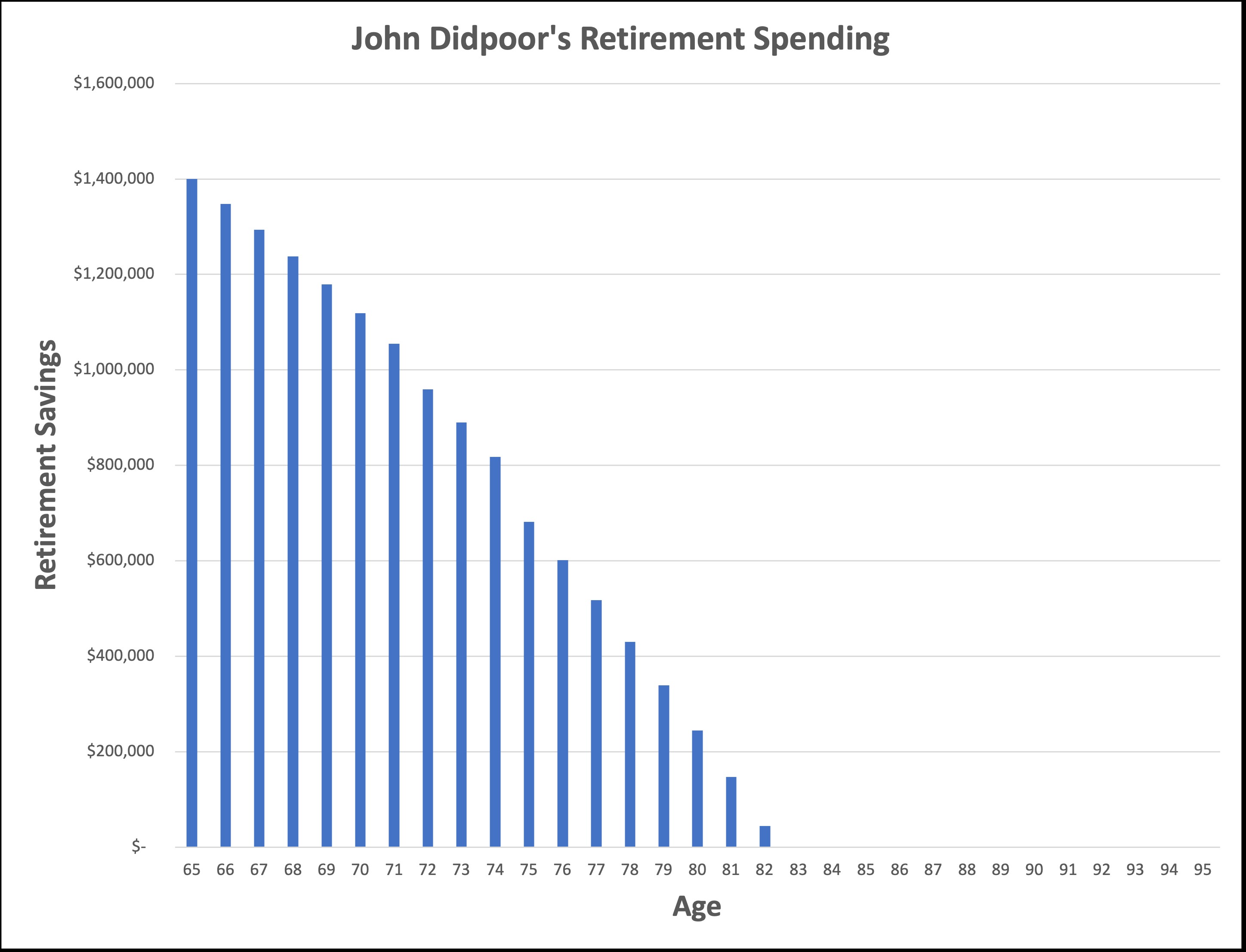

John Didpoor did not create a careful plan and decided to withdraw $4,000 monthly, and an additional $80,000 each year. John Didpoor also decided to buy himself a new truck at 71, and a new pool at 74. John was so excited for retirement spending that his savings actually ran out at 82 years old. John did not plan well and had to determine a new method of income to support himself past 83 years old.

When creating a plan, one of the most important things to note from this example is how a little can go a long way. These three examples shed light on the importance of careful retirement spending and a well-devised plan. In comparing Jack Didgreat’s spending plan to Jill Didfair’s spending plan, the two do not seem much different. Jill Didfair only spent $500 more than Jack monthly and $5,000 annually, for a total of only $11,000 more than Jack each year of retirement. However, once Jill reached 95 years old she was out of money, and Jack still had $569,403 in savings. That difference is substantial! As articulated throughout these spending scenarios, it is incredibly important to make a plan for retirement spending before you realize you are in the same shoes as John Didpoor.

Contributed by Sam Bassett.